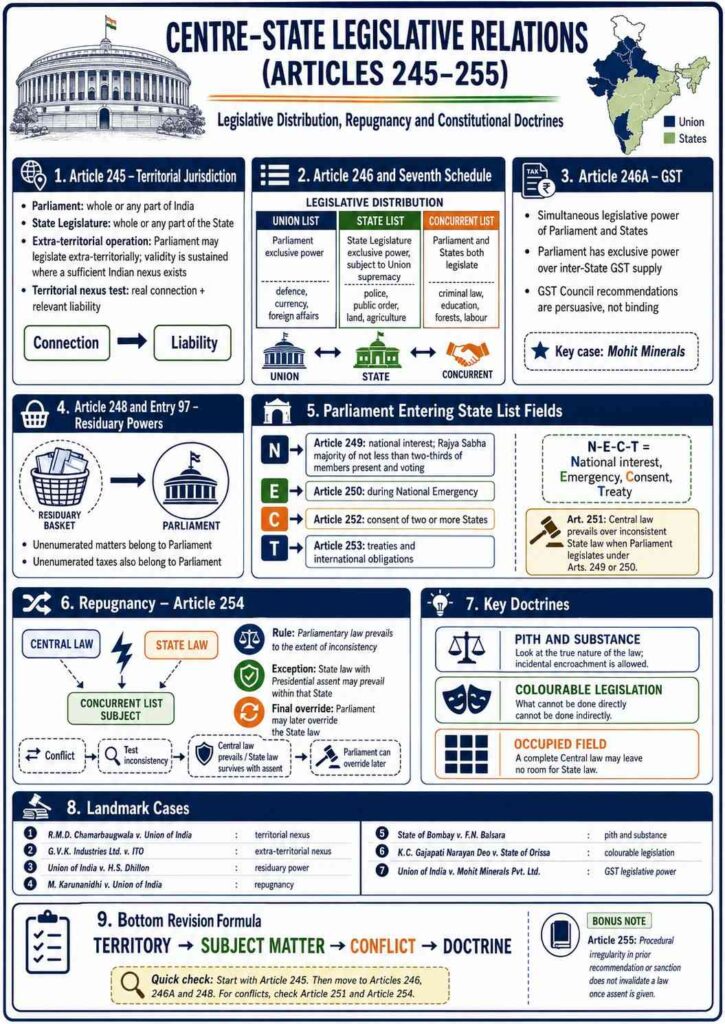

Constitutional Scheme of Centre–State Legislative Relations

🔹 Federal allocation: India has a federal constitutional structure with a comparatively strong Union. Legislative authority is divided by subject, territory and constitutional priority. Parliament and State Legislatures are not sovereign in the British sense; each must remain within the field assigned by the Constitution.

🔹 Three-stage validity test: When a law is challenged for lack of legislative competence, the enquiry should ordinarily proceed in this sequence:

| Question | Constitutional enquiry | Result |

|---|---|---|

| Territory | Can the legislature make a law having this territorial reach? | Article 245 and territorial nexus |

| Subject-matter | Does the law fall within the proper legislative entry? | Article 246, Article 246A, Article 248 and Seventh Schedule |

| Conflict | If both legislatures can legislate, do the laws clash? | Articles 251 and 254 |

🔹 Legislative entries: The entries in the Seventh Schedule are not independent sources of legislative power. Article 246 confers power; the entries identify the fields within which that power may operate. Entries are interpreted broadly, harmoniously and in a manner that avoids unnecessary overlap.

Territorial Jurisdiction under Article 245

Article 245: Extent of Laws

🔹 Parliament’s territory: Under Article 245(1), Parliament may make laws for the whole or any part of the territory of India. A State Legislature may make laws for the whole or any part of that State.

🔹 Extra-territorial operation: Article 245(2) provides that a Parliamentary law is not invalid merely because it has extra-territorial operation. Thus, Parliament may enact a law dealing with acts, persons, property or transactions outside India where they have a constitutionally sufficient connection with India.

🔹 State limitation: A State Legislature ordinarily legislates only for its own territory. However, a State law may affect persons, property or transactions outside its territory when there is a real territorial nexus between the State and the subject regulated.

⚖️ State of Bombay v. R.M.D. Chamarbaugwala, 1957 SCR 874 : AIR 1957 SC 699 — A prize-competition promoter operated through a newspaper printed outside Bombay, but the newspaper circulated in Bombay, entry forms and fees were received there, and local collectors operated within the State. The issue was whether Bombay could impose a tax despite the promoter being outside the State. The Supreme Court held that a State law can validly have extra-territorial effects if the connection is real rather than illusory and the liability imposed is relevant to that connection. The case establishes the two-part territorial nexus test: real nexus and relevance of liability to that nexus.

⚖️ G.V.K. Industries Ltd. v. Income Tax Officer, (2011) 4 SCC 36 — An Indian company challenged the application of income-tax provisions to payments made to a foreign consultant in connection with foreign financing arrangements. The constitutional issue was whether Parliament could legislate concerning extra-territorial matters. The Supreme Court held that Article 245(2) permits extra-territorial operation, but Parliament cannot legislate “for” a foreign territory having no connection with India. Parliament may regulate extra-territorial aspects only where those aspects have an impact, effect or sufficient nexus with India.

🔹 Practical distinction: Extra-territorial operation is permissible for Parliament; extra-territorial legislation having no Indian nexus is not. For States, territorial nexus is essential whenever the legislation substantially affects matters beyond State borders.

Subject-Matter of Laws under Article 246

Union List, State List and Concurrent List

🔹 Union List — Article 246(1): Parliament has exclusive power over matters in List I. Important examples include defence, foreign affairs, citizenship, currency, banking, communications, atomic energy and inter-State trade.

🔹 Concurrent List — Article 246(2): Parliament and State Legislatures may both legislate on List III subjects, subject to Parliament’s supremacy under Article 254. Important examples include criminal law, criminal procedure, marriage and divorce, contracts, evidence, forests, education, labour welfare and economic planning.

🔹 State List — Article 246(3): Subject to Union and Concurrent List powers, State Legislatures have exclusive authority over List II subjects. Important examples include public order, police, public health, agriculture, land, local government, markets, fairs and betting and gambling.

🔹 Union Territory power — Article 246(4): Parliament may legislate for Union Territories even on matters appearing in the State List. This is because Union Territories do not possess the constitutional status of States for purposes of Article 246.

| List | Primary Legislature | Typical subjects | Constitutional priority |

|---|---|---|---|

| List I — Union List | Parliament | Defence, currency, foreign affairs, railways | Highest under Article 246(1) |

| List II — State List | State Legislature | Police, land, public order, agriculture | Subject to Lists I and III |

| List III — Concurrent List | Parliament and States | Criminal law, education, forests, labour | Subject to Article 254 |

🔹 Broad interpretation: Legislative entries must receive the widest reasonable interpretation. Courts first try to reconcile apparently overlapping entries through harmonious construction. Only where reconciliation fails does the court examine the dominant character of the law through doctrines such as pith and substance.

🔹 Taxation distinction: A power to regulate a subject does not automatically include a power to tax it. Taxing entries are distinct and must be specifically located in the relevant legislative list.

⚖️ State of West Bengal v. Kesoram Industries Ltd., (2004) 10 SCC 201 — Several State levies and cesses connected with coal-bearing land, tea estates, brick earth and minerals were challenged. The issue was whether the State had entered a field reserved to Parliament concerning mineral regulation. The Supreme Court explained that legislative entries are fields of legislation requiring harmonious construction and that taxation is a distinct subject. A general regulatory entry cannot ordinarily be used to imply a power to impose a tax; taxing power must be traced to a specific taxation entry.

Article 246A: Special Legislative Power for GST

🔹 GST framework: Article 246A was inserted by the Constitution (One Hundred and First Amendment) Act, 2016. It creates a special and independent source of power for laws relating to goods and services tax.

🔹 Simultaneous power: Parliament and State Legislatures may both legislate on GST under Article 246A(1). This differs from ordinary Concurrent List power because Article 246A overrides Articles 246 and 254.

🔹 Inter-State supply: Under Article 246A(2), Parliament alone has exclusive power to legislate on GST where the supply takes place in the course of inter-State trade or commerce.

⚖️ Union of India v. Mohit Minerals Pvt. Ltd., (2022) 10 SCC 700 — The case concerned GST on ocean freight in cost-insurance-freight import transactions. While examining the GST constitutional structure, the Supreme Court held that Article 246A gives Parliament and State Legislatures a unique simultaneous law-making power over GST. Article 254 does not provide the ordinary repugnancy rule for GST laws. The Court further held that GST Council recommendations are recommendatory and persuasive, not binding legislative commands upon Parliament or State Legislatures.

Article 247: Additional Courts for Union List Laws

🔹 Additional courts: Article 247 authorises Parliament to establish additional courts for better administration of laws made by Parliament or existing laws concerning matters in the Union List.

🔹 Limited purpose: This is a specific power linked to Union List legislation. It does not create a general power to reorganise the entire State judicial structure.

Residuary Legislative Powers under Article 248 and Entry 97

🔹 Meaning: Residuary power concerns matters not enumerated in either the State List or the Concurrent List.

🔹 Parliament’s exclusive power: Article 248 gives Parliament exclusive power to legislate on such unenumerated matters. It also includes the power to impose a tax not mentioned in List II or List III.

🔹 Entry 97, List I: Entry 97 reinforces Article 248 by assigning “any other matter” not found in Lists II or III, including unenumerated taxes, to Parliament.

🔹 GST qualification: After the 101st Constitutional Amendment, Article 248 is expressly subject to Article 246A. Therefore, GST matters must first be considered under the special GST framework.

⚖️ Union of India v. H.S. Dhillon, (1971) 2 SCC 779 : (1972) 2 SCR 33 : AIR 1972 SC 1061 — The Finance Act, 1969 included agricultural land while computing net wealth for wealth-tax purposes. The challenge was that taxes on land were within State List Entry 49 and Parliament therefore lacked competence. The Supreme Court upheld the law, holding that where a matter, including a tax, is not assigned to List II or List III, Parliament may legislate under Article 248 read with Entry 97 of List I. The Court clarified that, in assessing a Central law, the essential question is whether it invades a prohibited State List field.

Parliament Legislating on State List Matters

Article 249: National Interest

🔹 Rajya Sabha resolution: Parliament may legislate on a State List matter if the Rajya Sabha passes a resolution, supported by not less than two-thirds of members present and voting, declaring that such legislation is necessary or expedient in the national interest.

🔹 Duration: The resolution remains valid for a period not exceeding one year, but may be renewed for further periods of up to one year each.

🔹 Effect after expiry: A law made under Article 249 ceases to have effect six months after the resolution expires, except regarding acts already done or omitted before expiry.

Article 250: National Emergency

🔹 Emergency power: While a Proclamation of Emergency is in operation, Parliament may legislate on any State List matter for the whole or any part of India.

🔹 Post-emergency effect: Such legislation ceases to operate six months after the Emergency ends, except for past acts and liabilities.

Article 251: Priority of Parliamentary Law

🔹 Temporary supremacy: Articles 249 and 250 do not remove State legislative power. States may continue legislating on their fields.

🔹 Conflict rule: Where a State law conflicts with a Parliamentary law made under Article 249 or 250, the Parliamentary law prevails. The State law remains inoperative only to the extent of inconsistency and only for as long as the Parliamentary law remains effective.

Article 252: Consent of Two or More States

🔹 State initiative: Where two or more State Legislatures resolve that Parliament should legislate on a State List matter, Parliament may enact a law for those States.

🔹 Adoption: Other States may later adopt the same Parliamentary law through a legislative resolution.

🔹 Amendment or repeal: A law made under Article 252 can be amended or repealed only by Parliament, not by the Legislature of an individual participating State.

Article 253: International Agreements

🔹 Treaty implementation: Parliament may legislate for the whole or any part of India to implement a treaty, agreement, convention, or decision of an international conference, association or body.

🔹 Override of State List: Article 253 operates notwithstanding the earlier provisions of Chapter I. Therefore, Parliament may legislate even on matters otherwise falling within the State List where implementation of an international obligation requires it.

⚖️ Maganbhai Ishwarbhai Patel v. Union of India, 1969 SCR (3) 254 : AIR 1969 SC 783 — The dispute arose from the Indo-Pakistan Western Boundary case concerning the Rann of Kutch. The issue included the constitutional mechanism for implementing international arrangements and the distinction between settlement of a boundary dispute and cession of Indian territory. The Supreme Court explained that Article 253 recognises Parliament’s exclusive law-making authority for implementing international agreements. It also reaffirmed that actual cession of territory forming part of India requires a constitutional amendment, whereas settlement of a boundary dispute may stand on a different footing.

Memory Aid: Exceptional Union Entry into State Fields

| Provision | Trigger word | Basis |

|---|---|---|

| Article 249 | National interest | Rajya Sabha resolution |

| Article 250 | Emergency | Proclamation of Emergency |

| Article 252 | Consent | Resolution by two or more States |

| Article 253 | Treaty | International obligation |

Repugnancy under Article 254

Meaning and Scope of Repugnancy

🔹 Core principle: Repugnancy arises when a valid State law conflicts with a valid Parliamentary law on the same Concurrent List matter.

🔹 Article 254(1): Where a State law is repugnant to a Parliamentary law, or an existing law, concerning a Concurrent List subject, the Parliamentary law prevails and the State law is void to the extent of repugnancy.

🔹 Same matter requirement: The two laws must operate upon substantially the same field. Mere similarity, overlap, allied purpose or incidental interaction is insufficient.

🔹 Article 254 and Lists I–II: Where a State law directly enters a Union List field, the issue is usually lack of legislative competence under Article 246, not repugnancy under Article 254.

Article 254(2): Presidential Assent

🔹 State exception: A State law on a Concurrent List subject that conflicts with an earlier Parliamentary law may prevail within that State if:

- it is reserved for the President’s consideration; and

- it receives Presidential assent.

🔹 Parliamentary override: Presidential assent does not permanently immunise the State law. Parliament may later enact a law adding to, amending, varying or repealing the State law. The later Parliamentary law prevails.

⚖️ M. Karunanidhi v. Union of India, (1979) 3 SCC 431 — The challenge concerned the Tamil Nadu Public Men (Criminal Misconduct) Act, 1973, which provided a special inquiry mechanism for allegations of criminal misconduct against public men. It was argued that the State law conflicted with the Indian Penal Code, the Prevention of Corruption Act, 1947 and the Criminal Procedure Code. The Supreme Court held that repugnancy requires a clear, direct and irreconcilable inconsistency such that obedience to one law necessarily means disobedience to the other. Since the State and Central laws differed in their scope, object and operational area, the Court found no repugnancy.

Tests for Repugnancy

🔹 Direct conflict: Are the provisions directly inconsistent?

🔹 Irreconcilability: Is the inconsistency incapable of reconciliation through harmonious interpretation?

🔹 Impossibility of simultaneous obedience: Can a person comply with both laws? If yes, repugnancy will ordinarily not arise.

🔹 Same field: Do the laws deal with the same matter, rather than merely cognate or related matters?

🔹 Parliamentary intention: Has Parliament clearly intended to create an exhaustive code occupying the entire field?

Doctrine of Occupied Field

🔹 Meaning: The doctrine of occupied field means that Parliament has enacted such a complete and exhaustive scheme on a Concurrent List subject that no room remains for State legislation in that field.

🔹 No automatic exclusion: Central legislation does not automatically exclude State law merely because both laws concern the same broad topic. The court must examine the actual scope, object and provisions of the Central statute.

🔹 Legislative vacuum: Where Parliament has regulated only part of a subject, States may still legislate in the remaining area, subject to Article 254.

⚖️ Ch. Tika Ramji v. State of Uttar Pradesh, 1956 SCR 393 : AIR 1956 SC 676 — The validity of the Uttar Pradesh Sugarcane (Regulation of Supply and Purchase) Act was challenged on the ground that Parliament had already legislated under the Industries (Development and Regulation) Act, 1951. The Supreme Court held that the Central law concerning the sugar industry did not occupy the separate field of sugarcane supply and purchase regulation. There was therefore no repugnancy. The case establishes that occupation of field must be determined from the true scope of Central legislation, not merely from the fact that Parliament has entered a related area.

⚖️ Vijay Kumar Sharma v. State of Karnataka, (1990) 2 SCC 562 — The case concerned the Karnataka Contract Carriages (Acquisition) Act and the Motor Vehicles Act, 1988. The Supreme Court explained that pith and substance is relevant when legislative competence is challenged, whereas repugnancy concerns whether an otherwise valid State law must yield to a conflicting Parliamentary law. The controlling enquiry is whether both laws can stand together, produce compatible results and operate in distinct fields.

Doctrine of Pith and Substance

🔹 Meaning: “Pith and substance” means the true nature, dominant character and essential subject-matter of legislation.

🔹 Purpose: The doctrine prevents a law from becoming invalid merely because it incidentally touches a matter assigned to another legislature.

🔹 Test: The court examines:

- Object of the legislation;

- Scheme and provisions of the statute;

- Practical effect and legal consequences;

- Dominant legislative field into which the law substantially falls.

🔹 Incidental trenching: If the law in its pith and substance falls within the enacting legislature’s field, incidental encroachment into another field does not invalidate it.

⚖️ State of Bombay v. F.N. Balsara, 1951 SCR 682 : AIR 1951 SC 318 — The Bombay Prohibition Act restricted possession, sale, transport and consumption of liquor, including foreign liquor. The argument was that the State had entered the Union field of import and export. The Supreme Court held that the Act was, in pith and substance, a law concerning intoxicating liquor, a State subject. Any effect on import was only incidental. The case remains the classic authority for the principle that incidental encroachment does not invalidate legislation whose dominant character lies within the legislature’s competence.

🔹 Limitation: Pith and substance cannot save a law where the apparent encroachment is actually substantial, direct and the dominant purpose of the enactment.

Doctrine of Colourable Legislation

🔹 Meaning: Colourable legislation arises where a legislature apparently acts within its constitutional field but, in substance and reality, does something beyond its power.

🔹 Core maxim: What a legislature cannot do directly, it cannot do indirectly.

🔹 Not about motive: The doctrine does not ordinarily examine the political motive, honesty or bad faith of legislators. The real question is constitutional competence.

🔹 Substance over form: Courts look beyond the title, drafting language and apparent label of the statute to its real operation and effect.

⚖️ K.C. Gajapati Narayan Deo v. State of Orissa, 1954 SCR 1 : AIR 1953 SC 375 — Landholders challenged the Orissa Estates Abolition Act, 1952 and related taxation measures, alleging that the legislation was a disguised attempt to avoid constitutional limitations. The Supreme Court held that colourable legislation is fundamentally a question of legislative competence, not legislative motive. A statute is invalid only where the legislature has transgressed constitutional limits under the disguise of acting within its assigned field. The Court upheld the legislation because the State Legislature had the relevant constitutional power.

Pith and Substance versus Colourable Legislation

| Basis | Pith and Substance | Colourable Legislation |

|---|---|---|

| Main concern | Incidental overlap between legislative fields | Disguised transgression beyond legislative power |

| Question asked | What is the dominant character of the law? | Has the legislature indirectly done what it cannot directly do? |

| Usual effect | May validate incidental trenching | May invalidate a disguised exercise of power |

| Motive relevant? | No | No; competence is decisive |

Article 255: Procedural Requirements and Assent

🔹 Procedural cure: Article 255 provides that an Act is not invalid merely because a required recommendation or previous sanction was not obtained, provided the required constitutional authority later gave assent to the Act.

🔹 Purpose: The Article treats certain requirements of recommendation and previous sanction as procedural rather than absolute jurisdictional conditions.

🔹 Conditions: The curative effect depends upon assent by the appropriate authority:

- where the Governor’s recommendation was required, assent must be by the Governor or President;

- where the Governor’s previous sanction was required, assent must be by the Governor or President;

- where the President’s recommendation or previous sanction was required, assent must be by the President.

🔹 Illustration: In R.M.D. Chamarbaugwala, the Supreme Court recognised that Presidential assent could cure the absence of prior Presidential sanction required for the State legislation in question.

Consolidated Revision Map

🔹 Territory: Article 245 decides where a law may operate.

🔹 Subject: Article 246, Article 246A, Article 248 and the Seventh Schedule decide who may legislate.

🔹 Union supremacy: Union List has priority; Concurrent List is subject to Article 254.

🔹 State List exceptions: Parliament may enter State fields through Articles 249, 250, 252 and 253.

🔹 Conflict: Article 251 governs temporary conflict arising from Articles 249 and 250; Article 254 governs repugnancy on Concurrent List matters.

🔹 Doctrines: Pith and substance validates incidental overlap; colourable legislation prevents disguised excess of power; occupied field determines whether Parliament has left any room for State action.