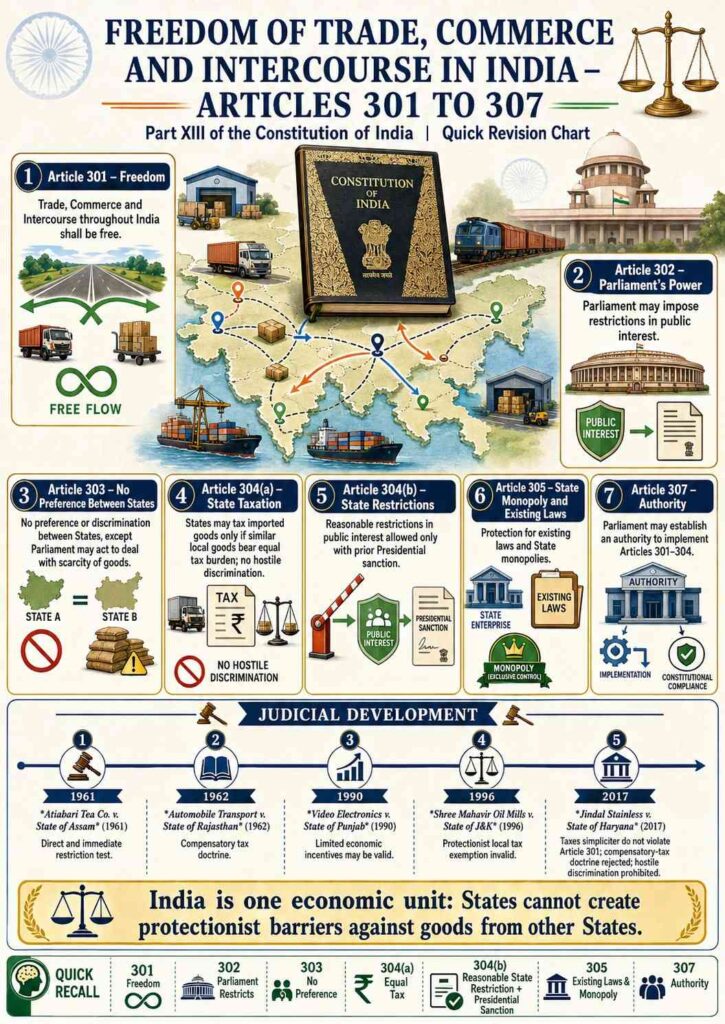

Constitutional Idea and Object of Part XIII

- National Economic Unity: Part XIII of the Constitution, containing Articles 301 to 307, seeks to maintain India as one integrated economic unit. It prevents States from creating protectionist barriers that fragment the national market into separate economic territories.

- Constitutional Guarantee: Article 301 declares that, “subject to the other provisions of this Part,” trade, commerce and intercourse throughout India shall be free. The freedom is therefore broad, but it is not absolute. Articles 302 to 305 expressly permit restrictions in defined situations.

- Nature of Right: Article 301 is not a Fundamental Right under Part III. It is a constitutional limitation on legislative power. A law may be validly enacted under Articles 245 and 246 read with the relevant entry in the Seventh Schedule, but can still be challenged if it violates Part XIII.

- Legislative Competence First: A challenge under Article 301 does not replace the question of legislative competence. A court must first ask whether Parliament or the State Legislature had power to enact the law. Even a non-discriminatory tax cannot survive if it is outside the legislature’s constitutional field of taxation.

- Relation with Article 19(1)(g): Article 19(1)(g) protects an individual citizen’s freedom to practise a profession or carry on trade or business. Article 301 protects the free flow of trade, commerce and intercourse across India. A measure may affect both provisions, but the constitutional tests and beneficiaries are different.

- Meaning of Trade, Commerce and Intercourse: These expressions receive a wide meaning. They cover commercial dealings, movement of goods, transportation, and movement connected with commercial activity. “Intercourse” is broader and may extend beyond a completed commercial transaction to movement and communication among different parts of India.

Structure of Articles 301 to 307

| Article | Subject | Core Rule |

|---|---|---|

| Article 301 | Freedom of trade, commerce and intercourse | Trade, commerce and intercourse throughout India shall be free, subject to Part XIII. |

| Article 302 | Parliament’s power | Parliament may impose restrictions in the public interest. |

| Article 303 | Ban on preference and discrimination | Parliament and States ordinarily cannot prefer one State over another or discriminate between States. |

| Article 304(a) | State taxation of imported goods | States may tax goods imported from other States or Union Territories, but cannot discriminate against them. |

| Article 304(b) | State non-tax restrictions | States may impose reasonable restrictions in the public interest, subject to prior Presidential sanction for the Bill or amendment. |

| Article 305 | Existing laws and State monopolies | Saves certain existing laws and laws relating to State monopolies under Article 19(6)(ii). |

| Article 306 | Former Part B States | Omitted by the Constitution (Seventh Amendment) Act, 1956. |

| Article 307 | Authority for Part XIII | Parliament may establish an authority to implement Articles 301–304. |

The present constitutional text shows that Article 301 is expressly made subject to the rest of Part XIII; Article 304 begins with a non-obstante clause overriding Articles 301 and 303 within its defined field.

Article 301: Freedom of Trade, Commerce and Intercourse

- General Rule: Article 301 protects free movement throughout India. It applies not merely to trade crossing State borders but also to trade occurring within a State, because the phrase used is “throughout the territory of India.”

- Direct and Immediate Effect Test: Historically, a law attracted Article 301 when its direct and immediate effect was to restrict the movement of trade. A remote, incidental or indirect economic effect was ordinarily insufficient.

- Restriction versus Regulation: A genuine regulatory measure may not violate Article 301 merely because it makes trade less convenient. For example, licensing, traffic regulation, safety conditions, inspection requirements and similar controls may be constitutionally valid where they regulate rather than directly obstruct trade. The substance and practical effect of the law, not its label, are decisive.

- Taxation after Jindal Stainless: The earlier position treated certain taxes as restrictions if they directly burdened movement. The present controlling position is that a tax simpliciter is not, by itself, a restriction under Part XIII. The word “free” in Article 301 does not mean freedom from every tax. A tax becomes constitutionally vulnerable under Part XIII when it is discriminatory in the protectionist sense.

Landmark Case: Atiabari Tea Co. Ltd. v. State of Assam, AIR 1961 SC 232; (1961) 1 SCR 809

- Facts, Issue and Ratio: Assam imposed a tax on goods carried by road or inland waterways, including tea transported through Assam to markets outside the State. Tea producers challenged the levy as a direct burden on movement of goods. The Supreme Court held that a tax law is not automatically excluded from Article 301. Where the tax directly and immediately restricts the movement of trade, it can offend Article 301 unless saved by another provision of Part XIII. The Court treated movement as an integral component of trade and held that the Assam levy had a direct and immediate restrictive effect. This case established the historic “direct and immediate effect” doctrine. Its treatment of taxes has later been limited by the nine-Judge Bench in Jindal Stainless, but the doctrine remains important for assessing non-tax restrictions.

Article 302: Parliament’s Power to Impose Restrictions

- Parliamentary Power: Article 302 authorises Parliament, by law, to impose restrictions on trade, commerce or intercourse between States, or within any part of India, when required in the public interest.

- Public Interest Standard: Article 302 does not use the phrase “reasonable restrictions.” Its text requires that the restriction be one required in the public interest. The law remains open to constitutional review for arbitrariness, lack of legislative competence, violation of Article 303, or other constitutional infirmities.

- Exclusive Nature: Article 302 empowers Parliament, not State Legislatures. A State cannot justify its own restriction under Article 302; its relevant constitutional source is Article 304.

- Central Sales Tax Context: Parliamentary taxation affecting inter-State trade may be sustained under Article 302, provided it is in public interest and does not violate Article 303.

Landmark Case: State of Madras v. N.K. Nataraja Mudaliar, AIR 1969 SC 147; (1968) 3 SCR 829

- Facts, Issue and Ratio: The validity of provisions of the Central Sales Tax Act, 1956 was challenged on the ground that varying rates connected with inter-State sales burdened inter-State trade and created unconstitutional preference. The Supreme Court rejected the challenge. It held that even assuming the Central Sales Tax had an impact on Article 301 freedom, it was a parliamentary law in the public interest and was protected by Article 302. The Court found no prohibited preference under Article 303. The case confirms that Parliament can regulate or burden inter-State trade through a valid law in the public interest, subject to Article 303.

Article 303: Prohibition on Preference and Discrimination Between States

- Basic Prohibition: Article 303(1) restrains both Parliament and State Legislatures. Despite Article 302, neither may make a law giving preference to one State over another, or discriminating between States, by virtue of an entry relating to trade and commerce in any list of the Seventh Schedule.

- Purpose: The provision prevents economic regionalism. A State cannot use legislative power to favour its own territory merely because local producers, consumers or traders would benefit.

- Scarcity Exception: Article 303(2) creates a narrow exception only for Parliament. Parliament may give preference or permit discrimination if the law declares that it is necessary to deal with scarcity of goods in any part of India.

- No Comparable State Exception: A State Legislature cannot invoke scarcity under Article 303(2). The exception belongs exclusively to Parliament and must be supported by a statutory declaration.

- Article 303 and Article 304(a): Article 303 is concerned with preference or discrimination between States. Article 304(a) specifically controls State taxation of goods imported from other States or Union Territories. In taxation disputes involving imported goods, Article 304(a) is generally the more direct provision.

Article 304(a): State Taxation and Non-Discrimination

- Permissive Power: Article 304(a) permits a State to impose a tax on goods imported from other States or Union Territories, provided similar goods manufactured or produced within that State bear a comparable tax burden.

- Core Requirement: The State must not discriminate between imported goods and locally manufactured or produced goods. The constitutional concern is protectionism, not every difference in tax treatment.

- Equality of Burden: The inquiry is not confined to whether the same statutory levy is imposed in identical words. Courts may examine the practical fiscal burden on imported goods and comparable local goods.

- No Presidential Sanction for Article 304(a): A tax law complying with Article 304(a) does not require prior Presidential sanction merely because it is a State tax measure. Prior sanction belongs to the separate field of Article 304(b).

- No Rescue through Article 304(b): A tax that violates Article 304(a) cannot be cured by satisfying Article 304(b) or by obtaining Presidential sanction. The two clauses operate independently.

Landmark Case: Firm A.T.B. Mehtab Majid & Co. v. State of Madras, AIR 1963 SC 928; [1963] Supp 2 SCR 435

- Facts, Issue and Ratio: The State imposed a higher sales tax burden on tanned hides and skins imported from outside the State than on similar locally processed goods. The issue was whether differential treatment of imported goods violated Article 304(a). The Supreme Court held that the tax was discriminatory because imported goods were placed at a fiscal disadvantage compared with similar local goods. The case established that a State cannot protect local industry through unequal tax treatment of goods coming from outside the State. The principle continues, though the later law emphasises hostile or protectionist discrimination rather than formal differentiation alone.

Landmark Case: State of Madhya Pradesh v. Bhailal Bhai, AIR 1964 SC 1006

- Facts, Issue and Ratio: Madhya Bharat imposed sales tax on imported tobacco while indigenous tobacco did not bear an equivalent levy. Dealers challenged the tax and sought refund. The Supreme Court held that the unequal treatment violated Article 304(a), because goods imported from another State were taxed while comparable local goods were not. The Court confirmed that Article 304(a) is a constitutional command against discriminatory taxation, not merely an administrative guideline.

Landmark Case: Video Electronics Pvt. Ltd. v. State of Punjab, (1990) 3 SCC 87

- Facts, Issue and Ratio: Punjab and Uttar Pradesh granted limited sales-tax incentives to specified new industrial units for a limited period. The challenge was that local incentives discriminated against goods coming from outside the State. The Supreme Court distinguished between ordinary differentiation and constitutionally prohibited discrimination. A time-bound incentive for a defined class of new industries, adopted as part of an economic-development policy, was not automatically hostile discrimination. The important principle is that every classification is not protectionism; however, the benefit must remain narrow, rational and non-colourable.

Landmark Case: Shree Mahavir Oil Mills v. State of Jammu and Kashmir, (1996) 11 SCC 39

- Facts, Issue and Ratio: Jammu and Kashmir granted complete sales-tax exemption to local edible-oil industries for ten years, while edible oil imported from other States was taxed at 8%. The Supreme Court struck down the exemption as discriminatory under Article 304(a). It held that the limited exception recognised in Video Electronics could not be expanded until it consumed the constitutional rule against protectionism. A broad, unconditional advantage for local producers, coupled with a burden on imported goods, is unconstitutional.

Article 304(b): Reasonable State Restrictions in Public Interest

- Field of Operation: Article 304(b) allows a State Legislature to impose reasonable restrictions on freedom of trade, commerce or intercourse with or within that State, where required in the public interest.

- Three Essential Conditions: A restriction under Article 304(b) must satisfy three conditions: it must be imposed by State law; it must be reasonable; and it must be required in the public interest.

- Prior Presidential Sanction: No Bill or amendment for purposes of Article 304(b) may be introduced or moved in a State Legislature without previous Presidential sanction. This is a mandatory constitutional condition precedent.

- Reasonableness Inquiry: The court examines the nature of the restriction, its degree, its public purpose, the connection between the measure and that purpose, and whether it operates excessively or arbitrarily. A restriction cannot be sustained merely because the State calls it regulatory.

- Independent Clause: After Jindal Stainless, clauses (a) and (b) of Article 304 are to be read disjunctively. Article 304(a) controls discriminatory taxation on imported goods; Article 304(b) governs reasonable non-tax restrictions in public interest.

- Practical Distinction: A State law imposing a non-discriminatory tax does not ordinarily need Article 304(b) approval. A State law imposing a direct restriction, such as a prohibition, quota, movement restraint or trading condition, must satisfy Article 304(b) where Article 301 is attracted.

Compensatory Taxes: Historical Doctrine and Present Position

- Historical Meaning: A compensatory tax was historically described as a levy imposed in return for the use of trading facilities, such as roads, bridges or transport infrastructure. The idea was that a trader who uses public facilities may bear a reasonable charge for them.

Landmark Case: Automobile Transport (Rajasthan) Ltd. v. State of Rajasthan, AIR 1962 SC 1406; (1963) 1 SCR 491

- Facts, Issue and Ratio: Motor transport operators challenged the Rajasthan motor-vehicle tax as violating Article 301. The Supreme Court upheld the levy on the ground that it was compensatory or regulatory in nature and related to road facilities used by transport operators. The Court developed the “working test”: a levy connected with facilities used by trade could be treated as outside Article 301 because it facilitated rather than obstructed trade. This became the foundation of the compensatory-tax doctrine, though it is no longer the governing test after the nine-Judge Bench decision in Jindal Stainless.

- Expansion of Doctrine: In Bhagatram Rajeevkumar v. Commissioner of Sales Tax, M.P., 1995 Supp (1) SCC 673, and State of Bihar v. Bihar Chamber of Commerce, (1996) 9 SCC 136, the Court adopted a broad “some connection” approach between the levy and facilities provided to trade. This diluted the earlier requirement of a meaningful compensatory link.

Landmark Case: Jindal Stainless Ltd. v. State of Haryana, (2006) 7 SCC 241

- Facts, Issue and Ratio: Challenges to State entry-tax laws raised the question whether the broad “some connection” test in Bhagatram Rajeevkumar and Bihar Chamber of Commerce was correct. The Constitution Bench held that the broad test was not good law and restored a stricter approach to compensatory taxation. However, the broader constitutional questions relating to taxes and Article 301 were later considered by a larger Bench.

Landmark Case: Jindal Stainless Ltd. v. State of Haryana, (2017) 12 SCC 1

- Facts, Issue and Ratio: A nine-Judge Bench considered the constitutional validity of entry-tax laws and revisited the doctrines developed in Atiabari Tea, Automobile Transport and the earlier Jindal Stainless decisions. By majority, the Court held that taxes simpliciter are not within Part XIII and Article 301 does not mean freedom from taxation. It held that only discriminatory taxes offend Article 304(a); Article 304(a) and 304(b) are disjunctive; a violation of Article 304(a) cannot be saved through Article 304(b); and the compensatory-tax doctrine has no juristic basis and stands rejected. The Court further held that Article 304(a) prohibits hostile, protectionist discrimination and not every differentiation, thereby preserving limited and non-hostile development incentives for specified classes or backward areas.

- Present Legal Position: The compensatory-tax doctrine is important only as judicial history. It is no longer necessary for a State to prove that a non-discriminatory tax is compensatory. The decisive question is whether the tax discriminates against imported goods or creates a hostile protectionist barrier. The Supreme Court has continued to treat the nine-Judge Bench ruling as the governing position on Article 301 and non-discriminatory taxes.

Article 305: Existing Laws and State Monopolies

- Saving Provision: Article 305 protects certain existing laws from challenge under Articles 301 and 303, subject to the President’s power to direct otherwise.

- State Monopoly Protection: Article 305 also protects laws relating to matters mentioned in Article 19(6)(ii), namely laws enabling the State, or a State-owned or State-controlled corporation, to carry on trade, business, industry or service, whether wholly or partially excluding citizens.

- Purpose: A State monopoly may inevitably restrict private commercial activity. Article 305 ensures that Article 301 cannot automatically invalidate a constitutionally authorised State monopoly.

- Historical Development: The State-monopoly protection must be read with Article 19(6)(ii), which was introduced after early litigation concerning State monopolies. Article 305 was substituted by the Constitution (Fourth Amendment) Act, 1955.

Landmark Case: Saghir Ahmad v. State of Uttar Pradesh, AIR 1954 SC 728; (1955) 1 SCR 707

- Facts, Issue and Ratio: Private bus operators challenged the Uttar Pradesh Road Transport Act, which enabled the State to establish a monopoly over road transport services. At that time, Article 19(6) did not expressly protect State monopolies. The Supreme Court held that the statutory scheme violated the freedom to carry on business under Article 19(1)(g). The case is historically important because it demonstrated the need for express constitutional protection for State monopolies. Article 19(6)(ii) and the later expanded wording of Article 305 provide that protection within their constitutional field.

Articles 306 and 307

- Article 306 — Omitted Provision: Article 306 originally gave certain powers to the former Part B States concerning restrictions on trade and commerce. It was omitted by the Constitution (Seventh Amendment) Act, 1956, following reorganisation of States. It has no present operative role.

- Article 307 — Implementing Authority: Parliament may appoint an authority to carry out the purposes of Articles 301 to 304 and may confer necessary powers and duties upon it. Article 307 is enabling; it does not itself establish a permanent constitutional authority.

Quick Revision Framework

| Question | Constitutional Route |

|---|---|

| Is there legislative competence to enact the measure? | Articles 245–246 and Seventh Schedule must first be satisfied. |

| Does the measure directly restrict trade, commerce or intercourse? | Article 301 may be attracted. |

| Is it a parliamentary restriction in public interest? | Examine Article 302, subject to Article 303. |

| Does it give preference to a State or discriminate between States? | Examine Article 303; scarcity exception belongs only to Parliament. |

| Is it a State tax on imported goods? | Examine Article 304(a): no hostile discrimination. |

| Is it a State non-tax restriction? | Examine Article 304(b): public interest, reasonableness and prior Presidential sanction. |

| Is it a State monopoly or an existing saved law? | Examine Article 305 read with Article 19(6)(ii). |

| Is the argument based on compensatory tax? | Apply Jindal Stainless; compensatory-tax theory is rejected. |

Core Principles to Remember

- Freedom: Article 301 creates the constitutional presumption of a free national market.

- Parliament: Article 302 permits Parliament to restrict trade in the public interest.

- Preference: Article 303 generally prohibits preference or discrimination between States; Parliament alone may depart from this rule to deal with scarcity.

- State Taxation: Article 304(a) permits State taxation but forbids hostile discrimination against imported goods.

- State Restrictions: Article 304(b) permits reasonable restrictions in public interest only with prior Presidential sanction for the Bill or amendment.

- Monopolies: Article 305 protects existing laws and constitutionally authorised State monopolies.

- Current Tax Rule: After Jindal Stainless, non-discriminatory taxes do not violate Article 301 merely because they burden trade.

- Protectionism Test: The constitutional vice is not every economic distinction; it is hostile or protectionist discrimination that places outside goods at an unfair disadvantage.