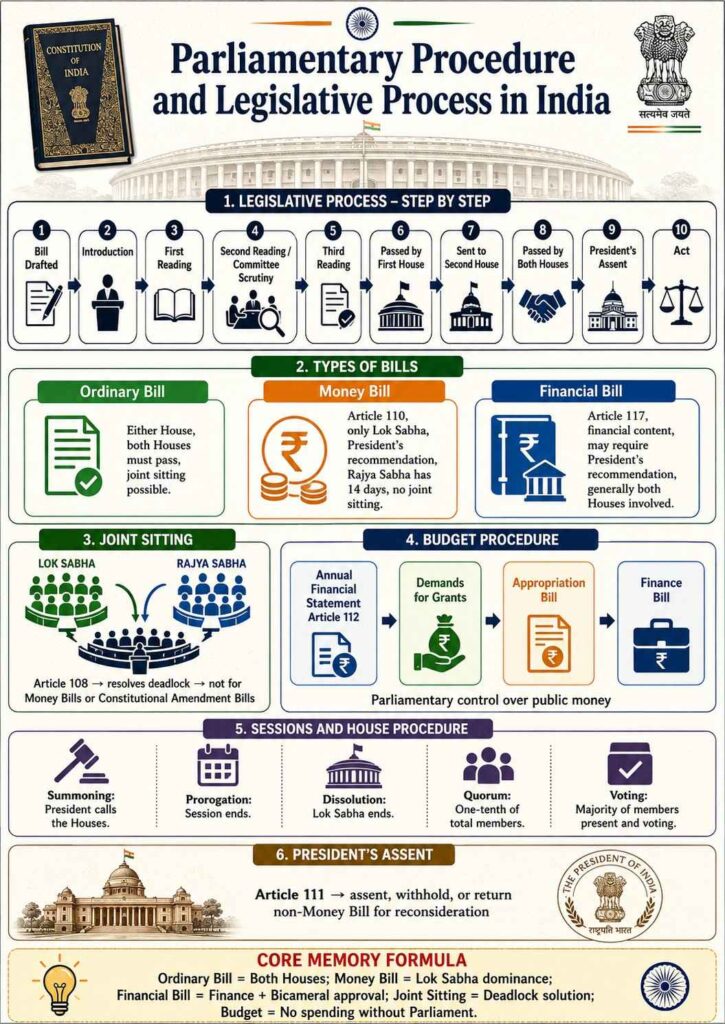

Introduction: Meaning and Constitutional Scheme of Parliamentary Procedure

• Parliamentary procedure means the constitutional and procedural method through which Parliament conducts its business, debates public issues, makes laws, controls public finance, and holds the executive accountable. In India, Parliament consists of the President, Lok Sabha and Rajya Sabha under Article 79 of the Constitution. The President is not a member of either House, but is an essential part of Parliament because no Bill becomes law without Presidential assent under Article 111. The legislative procedure is mainly contained in Articles 107 to 122, while the financial procedure is mainly contained in Articles 112 to 117 of the Constitution.

• Democratic purpose of parliamentary procedure is to ensure that law-making is not arbitrary. A Bill generally has to be introduced, debated, examined, voted upon, passed by both Houses, and then presented to the President. This process gives space for deliberation, opposition, amendment, financial scrutiny and constitutional supervision.

• Bicameral balance is a central feature of Parliament. Lok Sabha represents the people directly, while Rajya Sabha represents the States and Union territories in the federal structure. However, in financial matters, the Constitution gives a stronger position to Lok Sabha because taxation and expenditure are treated as matters of popular control.

• Constitutional discipline is maintained by several provisions: Articles 85 to 88 deal with sessions, prorogation, dissolution, and Presidential address; Article 100 deals with voting and quorum; Articles 107 to 111 deal with Bills and assent; Articles 112 to 117 deal with budget and financial legislation; Articles 118 to 122 deal with rules of procedure, language, restriction on discussion about judges, and limited judicial interference in parliamentary proceedings.

Sessions of Parliament, Summoning, Prorogation and Dissolution

• Session of Parliament means the period during which a House meets to conduct business. Under Article 85, the President summons each House from time to time, but six months shall not intervene between the last sitting of one session and the first sitting of the next session. This means Parliament must meet at least twice a year, though in practice it usually has Budget, Monsoon and Winter sessions.

• Summoning means calling the House to meet. The formal power is with the President under Article 85, but in a parliamentary system this power is exercised on the aid and advice of the Council of Ministers.

• Prorogation means termination of a session of a House by the President. It does not dissolve the House. A prorogued House continues to exist; only that session ends. Under Article 107(3), a Bill pending in Parliament does not lapse merely because the Houses are prorogued.

• Adjournment is different from prorogation. Adjournment only suspends the sitting of a House for a specified time, such as a few hours, a day, or a week. It is done by the Presiding Officer, not by the President.

• Dissolution applies only to Lok Sabha, not Rajya Sabha. Rajya Sabha is a permanent House and is not subject to dissolution. Lok Sabha may be dissolved either on expiry of its five-year term or earlier. Dissolution has serious consequences for pending Bills, because the directly elected House ceases to exist.

• Effect on pending Bills under Article 107 is important. A Bill pending in Rajya Sabha which has not been passed by Lok Sabha does not lapse on dissolution of Lok Sabha. But a Bill pending in Lok Sabha, or a Bill passed by Lok Sabha and pending in Rajya Sabha, lapses on dissolution of Lok Sabha, subject to Article 108 on joint sitting.

• Purushothaman Nambudiri v. State of Kerala, AIR 1962 SC 694; 1962 Supp (1) SCR 753: The case concerned the effect of dissolution and lapse of Bills in the context of legislative procedure. The Supreme Court explained that the Constitution rejects the old English rule that all pending Bills lapse merely because of prorogation, and instead specifically provides when lapse occurs. The ratio is that lapse is governed by the constitutional text, not by general assumptions from British parliamentary practice. This principle helps understand Articles 107 and 196, which separately deal with Parliament and State Legislatures.

Quorum, Voting and Decision-Making in Parliament

• Quorum means the minimum number of members required to be present for a valid sitting of a House. Under Article 100(3), the quorum to constitute a meeting of either House of Parliament is one-tenth of the total number of members of that House. If quorum is not present, the Presiding Officer must either adjourn the House or suspend the meeting until quorum is present.

• Voting rule under Article 100(1) is that all questions in either House, or in a joint sitting, are decided by a majority of votes of the members present and voting, unless the Constitution provides otherwise. The Presiding Officer generally does not vote in the first instance but has a casting vote in case of equality of votes.

• Present and voting means only those members who are actually present and cast their vote are counted. Members who are absent or abstain are not counted for deciding the majority, unless a special constitutional provision requires a majority of the total membership or a special majority.

• Ordinary majority is the usual rule for passing ordinary Bills and many motions. However, constitutional amendment Bills under Article 368 require special majority, and in some cases ratification by at least half of the State Legislatures.

• Voice vote and division are parliamentary methods of voting. In a voice vote, members say “Ayes” or “Noes”, and the Presiding Officer decides which side is stronger. If the decision is challenged, a division may be demanded, where votes are counted more formally.

Ordinary Bills: Meaning, Introduction and Passing

• Ordinary Bill means a Bill which is not a Money Bill, not a Financial Bill requiring special procedure, and not a constitutional amendment Bill. It may relate to subjects such as criminal law, civil law, administration, social welfare, institutions, regulatory bodies or rights.

• Article 107 rule is that, subject to provisions relating to Money Bills and Financial Bills, an ordinary Bill may originate in either House of Parliament. It can be introduced in Lok Sabha or Rajya Sabha. It is not deemed to have been passed by Parliament unless both Houses agree to it, either without amendment or with amendments accepted by both Houses.

• First reading is the introduction stage. The Minister or private member seeks leave to introduce the Bill. After introduction, the Bill is published. At this stage, there is usually no detailed debate on the merits of the Bill.

• Second reading is the most important deliberative stage. It usually includes general discussion, possible reference to a Department-related Parliamentary Standing Committee or Select Committee, clause-by-clause consideration, and amendments. This stage allows members to examine the purpose, structure, language and consequences of the Bill.

• Committee scrutiny improves legislative quality. Committees examine the Bill more closely, may hear experts and stakeholders, and suggest changes. Though committee recommendations are generally not binding, they are important for informed law-making.

• Third reading is the final stage in the House where the Bill is put to vote. Debate is usually limited to whether the Bill should be passed in its final form.

• Transmission to the other House occurs after one House passes the Bill. The other House may pass it without amendment, pass it with amendments, reject it, or take no action. For ordinary Bills, both Houses must ultimately agree.

• Deadlock possibility arises when one House passes a Bill and the other House rejects it, disagrees with amendments, or does not pass it for more than six months. In such cases, Article 108 may allow a joint sitting, except for Bills excluded from joint sitting.

Joint Sitting under Article 108

• Joint sitting is a constitutional method for resolving deadlock between Lok Sabha and Rajya Sabha on certain Bills. Under Article 108, the President may notify the intention to summon both Houses to meet in a joint sitting where: the Bill is rejected by the other House; the Houses finally disagree on amendments; or more than six months pass from the date of receipt of the Bill by the other House without passage.

• Purpose of joint sitting is to prevent legislative paralysis. Since Lok Sabha has a larger membership than Rajya Sabha, the will of Lok Sabha usually carries greater weight in a joint sitting. However, Rajya Sabha members also participate and vote.

• Presiding authority is ordinarily the Speaker of Lok Sabha. In the Speaker’s absence, the Deputy Speaker or other constitutionally/rule-authorised person presides.

• Bills excluded from joint sitting include Money Bills and Constitutional Amendment Bills. Money Bills have a special Lok Sabha-dominant process under Articles 109 and 110. Constitutional amendment Bills under Article 368 must be passed separately by each House with the required special majority; there is no joint sitting for them.

• Dissolution after notification does not necessarily defeat a joint sitting. Article 108(5) provides that a joint sitting may be held and the Bill may be passed even if dissolution of Lok Sabha has intervened after the President has notified the intention to summon a joint sitting.

• Historical use has been rare. Joint sittings have been used for the Dowry Prohibition Bill, 1959; the Banking Service Commission (Repeal) Bill, 1977; and the Prevention of Terrorism Bill, 2002. PIB records that the Dowry Prohibition Bill was passed at a joint sitting on 9 May 1961, and the Banking Service Commission (Repeal) Bill was passed at a joint sitting in May 1978.

Money Bills under Articles 109 and 110

• Money Bill is a special category of Bill dealing only with the matters listed in Article 110(1). A Bill is a Money Bill if it contains only provisions dealing with matters such as taxation, government borrowing, custody of the Consolidated Fund or Contingency Fund of India, appropriation of money, declaration of expenditure charged on the Consolidated Fund, receipt or custody of public money, audit of accounts, or matters incidental to these subjects.

• Keyword “only” is extremely important. A Bill cannot become a Money Bill merely because it has some financial implication. It must contain only provisions dealing with the subjects mentioned in Article 110(1)(a) to (g). The incidental clause in Article 110(1)(g) cannot be used to include unrelated substantive matters.

• Speaker’s certificate under Article 110(3) is constitutionally significant. If any question arises whether a Bill is a Money Bill, the decision of the Speaker of Lok Sabha is final. The certificate is endorsed when the Bill is transmitted to Rajya Sabha and when it is presented to the President.

• Lok Sabha origin is compulsory. Under Article 109, a Money Bill cannot be introduced in Rajya Sabha. It can be introduced only in Lok Sabha, and only on the recommendation of the President.

• Rajya Sabha’s limited role means Rajya Sabha cannot reject or amend a Money Bill. It may only make recommendations within fourteen days from receipt. Lok Sabha may accept or reject all or any of those recommendations. If Rajya Sabha does not return the Bill within fourteen days, it is deemed to have been passed by both Houses in the form passed by Lok Sabha.

• No joint sitting is available for a Money Bill because the Constitution gives a special final say to Lok Sabha.

• K.S. Puttaswamy v. Union of India, (2019) 1 SCC 1 / Aadhaar Constitution Bench: The Aadhaar Act was challenged, including on the ground that it was wrongly passed as a Money Bill. The majority upheld the certification, reasoning that the core of the Act related to targeted delivery of subsidies and benefits involving expenditure from the Consolidated Fund of India. Justice D.Y. Chandrachud dissented and held that passing the Aadhaar Act as a Money Bill was constitutionally improper. The case is important because it exposed the controversy around the breadth of Article 110.

• Rojer Mathew v. South Indian Bank Ltd., (2020) 6 SCC 1 / 2019 SCC OnLine SC 1456: The Supreme Court considered whether provisions relating to tribunals could be passed through a Finance Act certified as a Money Bill. The Court doubted the correctness of the Aadhaar majority’s approach to Article 110 and referred the larger question of interpretation of Money Bills to a larger Bench. The key principle emerging from the reasoning is that Article 110 must be read carefully because the Money Bill route bypasses Rajya Sabha’s equal legislative role.

Financial Bills under Article 117

• Financial Bill is broader than a Money Bill. Every Money Bill is financial in nature, but every Financial Bill is not a Money Bill.

• Article 117(1) Financial Bill contains matters mentioned in Article 110 along with other matters. It can be introduced only in Lok Sabha and only on the President’s recommendation. But unlike a Money Bill, Rajya Sabha has full legislative powers over it because it is not confined only to Article 110 matters. Therefore, it must be passed by both Houses, and a joint sitting may be possible if a deadlock arises.

• Article 117(3) Financial Bill does not contain Article 110 matters but involves expenditure from the Consolidated Fund of India. It may be introduced in either House, but it cannot be passed unless the President has recommended its consideration. This is because it affects public expenditure.

• Practical distinction is simple: a Money Bill is Lok Sabha-controlled; an Article 117(1) Financial Bill begins only in Lok Sabha but needs approval of both Houses; an Article 117(3) Financial Bill may begin in either House but needs Presidential recommendation before passage.

Comparative Table: Ordinary Bill, Money Bill and Financial Bill

| Basis | Ordinary Bill | Money Bill | Financial Bill |

|---|---|---|---|

| Main Articles | Articles 107–108 | Articles 109–110 | Article 117 |

| House of origin | Either House | Only Lok Sabha | Article 117(1): only Lok Sabha; Article 117(3): either House |

| President’s recommendation | Generally not required | Required | Required as per Article 117 |

| Rajya Sabha power | Equal power | Only recommendations within 14 days | Generally full power, unless it is a Money Bill |

| Joint sitting | Possible | Not possible | Possible for Article 117(1), if deadlock arises |

| Speaker’s certificate | Not required | Required | Not required unless certified as Money Bill |

| Final passage | Both Houses must agree | Lok Sabha has final say | Both Houses generally must agree |

Presidential Assent under Article 111

• Assent stage begins after a Bill has been passed by Parliament. It is then presented to the President under Article 111.

• President’s options are: give assent, withhold assent, or return the Bill for reconsideration if it is not a Money Bill. If the Bill is returned and Parliament passes it again with or without amendments, the President shall not withhold assent.

• Money Bill exception is important. The President cannot return a Money Bill for reconsideration under Article 111. This is because a Money Bill is introduced only with the President’s prior recommendation.

• Constitutional role of assent is not merely ceremonial in theory, but in a parliamentary system the President generally acts on the aid and advice of the Council of Ministers. However, the assent stage remains constitutionally essential because a Bill becomes an Act only after assent.

• No express time limit is mentioned in Article 111 for Presidential assent. This has created constitutional debate about delays. The better constitutional understanding is that the power must be exercised within a reasonable constitutional framework, because indefinite inaction may defeat parliamentary law-making.

Budget and Annual Financial Statement

• Budget is the popular name for the Annual Financial Statement under Article 112. It is a statement of the estimated receipts and expenditure of the Government of India for a financial year. The Constitution uses the expression Annual Financial Statement, not “Budget”.

• Charged expenditure and voted expenditure are treated differently. Charged expenditure is charged upon the Consolidated Fund of India and is not submitted to vote, though it may be discussed. Examples include the salary and allowances of certain constitutional authorities and debt charges. Voted expenditure is submitted to Lok Sabha in the form of demands for grants.

• Demands for grants under Article 113 are presented to Lok Sabha. Rajya Sabha may discuss the Budget, but voting on demands for grants is the function of Lok Sabha. This shows the principle that the directly elected House controls public expenditure.

• Appropriation Bill under Article 114 authorises withdrawal of money from the Consolidated Fund of India. No money can be withdrawn from the Consolidated Fund except under appropriation made by law. The Appropriation Bill gives legal authority to spend.

• Finance Bill gives effect to taxation proposals. It usually contains proposals for imposition, abolition, remission, alteration or regulation of taxes. Depending on its contents, it may be a Money Bill or a Financial Bill.

• Supplementary, additional or excess grants under Article 115 are required when the authorised amount is insufficient, when a new service requires expenditure, or when money has been spent in excess of the amount granted.

• Vote on account under Article 116 allows the government to obtain parliamentary approval for expenditure for part of the financial year before the full budget process is completed. It is a practical device to keep administration running.

• Vote of credit under Article 116 is used for meeting an unexpected demand when the magnitude or indefinite character of the service makes detailed demand difficult, such as emergencies.

• Exceptional grant under Article 116 is granted for a special purpose not forming part of the current service of any financial year.

Parliamentary Control over Executive through Financial Procedure

• Financial accountability is the heart of parliamentary democracy. The executive cannot raise taxes or spend public money without parliamentary authority. This reflects the classic democratic principle: no taxation and no expenditure without legislative control.

• Lok Sabha’s supremacy in finance exists because the Council of Ministers is collectively responsible to Lok Sabha under Article 75(3). Since the government survives only while it enjoys Lok Sabha’s confidence, financial approval by Lok Sabha is politically decisive.

• Cut motions are tools through which members may seek reduction of demands for grants. They are used to criticise government policy, economy of expenditure or specific grievances. Even when not passed, they allow detailed scrutiny.

• Guillotine means putting outstanding demands for grants to vote at the appointed time without further discussion. It is used because the House has limited time to pass the Budget before the financial year begins.

• Public Accounts Committee, Estimates Committee and Committee on Public Undertakings strengthen financial oversight after money is authorised and spent. Parliamentary control is therefore both prior and subsequent.

Rules of Procedure, Language and Internal Autonomy

• Article 118 empowers each House of Parliament to make rules for regulating its procedure and conduct of business. Until such rules are made, rules from the pre-Constitution legislature may continue subject to modification.

• Article 120 deals with language to be used in Parliament. Business is transacted in Hindi or English, but the Presiding Officer may permit a member who cannot adequately express himself or herself in either language to address the House in the member’s mother tongue.

• Article 121 restricts discussion in Parliament regarding the conduct of judges of the Supreme Court or High Courts in discharge of their duties, except upon a motion for presenting an address to the President for removal of the judge.

• Article 122 protects parliamentary proceedings from being questioned in court on the ground of mere irregularity of procedure. It also protects parliamentary officers and members exercising procedural powers from court jurisdiction in respect of those powers. However, this does not create absolute immunity for unconstitutional acts.

• Raja Ram Pal v. Hon’ble Speaker, Lok Sabha, (2007) 3 SCC 184: The case arose after members of Parliament were expelled following allegations of accepting money for raising questions. The Supreme Court held that parliamentary proceedings are protected from judicial interference for procedural irregularities, but substantive illegality or unconstitutionality may be judicially reviewed. The ratio is that Indian Parliament is not sovereign in the British sense; it is controlled by the Constitution, and judicial review is part of the basic structure.

Doctrine of Lapse: When Bills Survive and When They Fail

• Prorogation rule is that a Bill pending in Parliament does not lapse merely because the House or Houses are prorogued. This ensures continuity of legislative business.

• Rajya Sabha pending Bill does not lapse on dissolution of Lok Sabha if it has not been passed by Lok Sabha. Since Rajya Sabha is permanent, such a Bill may continue.

• Lok Sabha pending Bill lapses when Lok Sabha is dissolved. The reason is that the House where the Bill was pending has ceased to exist.

• Bill passed by Lok Sabha and pending in Rajya Sabha also lapses on dissolution of Lok Sabha, subject to Article 108. This is because the new Lok Sabha must have the opportunity to reconsider legislative policy.

• Bill passed by both Houses and pending for President’s assent does not lapse because parliamentary passage is complete. At that stage, the legislative process has moved to the assent stage.

Memory Aid: Legislative Process Flow

| Stage | Ordinary Bill | Money Bill |

|---|---|---|

| Introduction | Either House | Only Lok Sabha |

| Recommendation of President | Usually not needed | Mandatory |

| Debate and passage in first House | Required | Required in Lok Sabha |

| Role of second House | Full power to pass, reject or amend | Rajya Sabha can only recommend |

| Deadlock solution | Joint sitting possible | No joint sitting |

| Assent | President may assent, withhold, or return | President may assent or withhold; cannot return |

| Becomes law | After assent | After assent |

Important Constitutional Principles to Remember

• Bicameralism with exceptions means both Houses generally participate equally in law-making, but Lok Sabha has primacy in money matters.

• Financial initiative of executive means taxation and expenditure proposals usually require Presidential recommendation, reflecting executive responsibility in public finance.

• Speaker’s Money Bill certificate is final in the internal parliamentary sense, but modern case law shows that courts may examine serious constitutional violations, especially where bicameralism is bypassed.

• Joint sitting is exceptional, not routine. It exists only to resolve deadlocks in ordinary legislative business and certain financial Bills, not Money Bills or Constitutional Amendment Bills.

• Assent completes law-making because a Bill, even if passed by both Houses, is not an Act until the President gives assent.

• Quorum and voting rules ensure that parliamentary decisions have minimum institutional participation and are decided by constitutionally recognised majorities.

• Judicial restraint and constitutional review coexist. Courts do not interfere with mere procedural irregularities inside Parliament, but they may intervene where there is substantive illegality, constitutional violation, or breach of fundamental constitutional limitations.

Conclusion: Essence of Parliamentary Procedure and Legislative Process

• Parliamentary procedure in India is a carefully balanced constitutional system. It combines democratic debate, federal bicameralism, executive financial responsibility, Lok Sabha’s popular mandate, Rajya Sabha’s revising role, Presidential assent, and limited judicial review.

• Ordinary Bills follow the normal bicameral route and require approval of both Houses. Money Bills are controlled mainly by Lok Sabha because they concern taxation and public money. Financial Bills stand between ordinary and Money Bills, depending on their contents. Joint sitting resolves deadlocks but is not available for Money Bills or constitutional amendments. Budget procedure ensures that the executive cannot tax or spend without legislative authority. Sessions, prorogation, dissolution, quorum and voting provide the working framework through which Parliament functions.

• Constitutional morality behind the process is that laws should be made after deliberation, public finance should remain accountable to elected representatives, and parliamentary autonomy should operate within the supremacy of the Constitution.